.png) 2 months ago

31

2 months ago

31

OBR warns UK public finances are in a vulnerable position

Newsflash: The UK public finances have fallen into a “relatively vulnerable position” and are facing mounting risks, the country’s fiscal watchdog is warning.

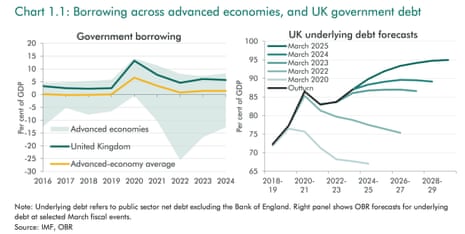

The Office for Budget Responsibility has just issued its latest Fiscal risks and sustainability report. It warns that the UK’s ability to respond to future shock has been substantially eroded, with underlying public debt is now at its highest level since the early 1960s and projected to rise further.

The OBR says:

Efforts to put the UK’s public finances on a sustainable footing after a series of global shocks have met with only limited and temporary success in recent years, leaving the UK with the sixth-highest debt, fifth-highest deficit, and third-highest borrowing costs among 36 advanced economies.

Against this more vulnerable backdrop, the risks to the fiscal outlook are mounting, including: the sustainability of state and private pensions and the sector’s demand for government debt; risks to assets and liabilities on the public balance sheet and the Government’s new net financial liabilities target; and the combined costs of climate damage and the net zero transition.

The OBR’s report paints a concerning position about the UK pubic finances, showing the challenge facing chancellor Rachel Reeves.

It points out that:

-

at the end of last year, the UK government’s deficit was 5.7% of GDP, around 4 percentage points higher than the advanced-economy average. This is the third highest among 28 advanced European economies, and the fifth highest among 36 advanced economies – after France, Slovakia, the US, and Israel.

-

At 94% of GDP, UK government debt is the fourth highest among advanced European economies, and the sixth highest among advanced economies (after Japan, Greece, Italy, France, and the US).

-

And with its 10-year bond yielding 4.5% at the end of June, the UK government faces the third-highest borrowing costs of any advanced economy after New Zealand and Iceland.

Key events Show key events only Please turn on JavaScript to use this feature

M&S chair says cyberattack was carried out by 'DragonForce'

Archie Norman then gives a broad outline of the M&S hack, telling MPs that the company believes the instigator of the cyberattack was a group called “DragonForce”.

The M&S chairman explains that attackers don’t send a letter announcing their identity, saying:

We didn’t even hear from the threat actor for approximately a week after they penetraded our systems.

Instead, security advisors “recognise the threat actor by the attack factor, in other words the pattern they use”, Norman explains.

The M&S attack has been previously linked to a hacking collective known as Scattered Spider.

Norman points out, though, that attackers works through intermediaries, explaining:

We believe there was the instigator of the attack, believed to be DragonForce, a ransom operation based we believe in Asia.

[DragonForce have been dubbed as “Ransomware-as-a-Service group”, who develop malware and lease it to affiliates].

Norman says M&S decided not to deal with the threat actor directly, and would leave that to the professionals.

Threat actors typically communicate through the media – in this case, principally through the BBC, he adds:

Norman says he’s sure the BBC handled this “completely properly”, adding:

“It was sometimes an usual experience to be brushing your teeth in the morning, when someone comes onto the BBC with a communnication from the people who are allegedly attacking your business.”

M&S chair: Cyber-attack was traumatic

Speaking of cyber-crime… Archie Norman, the chairman of Marks and Spencer, is telling MPs that the cyber-attack which disrupted the company’s operations this week was a “traumatic” experience for M&S.

Norman, a veteran retailer, has explained to a sub-committee of the Business and Trade committee that the attack was an “outer body” experience, which he could only compare to the shock and disruption of a hostile takeover bid.

He tells MPs:

“It’s very rare to have a criminal actor in another country, or in this country – we’re never quite sure – seeking to stop customers shopping at M&S.

Essentially trying to destroy your business, for purposes which are not entirely clear, but partly, undoubtely, ransom, extortion.

Norman then explains that everyone at M&S was affected by the attack, which was reported in mid-April.

Shop staff had to work in ways they’d not worked for 30 years, putting in extra hours to “keep the show on the road”.

While M&S’s cyber team probably only had three hours sleep a night, or none at all, for a week, Norman suggests, saying:

“It’s not an overstatement to describe it as traumatic. And it has endured some weeks.

We’re still in the rebuild mode, and we will be for some time to come.”

M&S reopened its website to shoppers on 1 June, after halting online orders for six weeks due to the attack, which is estimated to cost up to £300m in profits this year.

OBR: Cyber-attacks could hurt UK finances

Cyber-crime is another threat to the UK public finances, the OBR adds.

Its fiscal risks report points out that “a series of major cyber-attacks” have hit the UK this year, adding:

Cyber-attacks have continued to intensify, as evidenced by the recent attacks on the Legal Aid Agency, HMRC, and Marks & Spencer. We estimate that a cyberattack on critical national infrastructure has the potential to temporarily increase borrowing by 1.1 per cent of GDP.

That fiscal impact comes from increased government spending, such as emergency response and system recovery, and wider macroeconomic effects, including reduced tax receipts.

The UK’s pensions bill is set to keep rising sharply, the OBR points out:

Spending on the state pension has risen steadily over the past eight decades.

It rose from around 2 per cent of GDP in the mid-20th century to around 5 per cent of GDP (£138 billion) today, and is estimated to rise further to 7.7 per cent of GDP by the early 2070s in our central long-term projection.

OBR: public debt on track to hit 270% of GDP by the 2070s

The top line, long-term forecast from the Office for Budget Responsibility is that public debt is on track to hit 270% of GDP by the 2070s, based on current tax and spending policy settings.

That would be almost three times higher than its current level of around 95% of GDP.

The OBR says:

Over the long term, the demographic pressures of an ageing population and rising costs of healthcare and other age-related expenditures are still, on current policy settings, projected to push borrowing above 20 per cent and debt above 270 per cent of GDP by the early 2070s.

The OBR points out that UK national debt has been pushed up since 2010 by two major shocks – the Covid pandemic and the energy crisis.

It implicitely criticises recent chancellors for not tackling the resulting rise in underlying debt, saying:

The UK economy has been particularly hard hit by those shocks, and government support to affected firms and households has been relatively generous by international standards. But in the aftermath of the shocks, debt has also continued to rise and borrowing remained elevated because governments have reversed plans to consolidate the public finances.

Planned tax rises have been reversed, and, more significantly, planned spending reductions have been abandoned. The more persistent fiscal deficits and ratcheting up of debt that resulted have been accommodated by successive loosening of the fiscal rules.

The OBR is concerned that slowing the rise in UK public debt has become “more challenging” as economic growth has slowed and interest rates risen.

They warn:

Despite the tax-to-GDP ratio rising to the highest level in the period since 1950, borrowing is still 3 per cent of GDP above the level that would be needed to durably stabilise debt.

And the Government has left itself very small margins against its objectives of restoring the current budget to balance and getting net financial liabilities to fall by the end of the decade. Despite this, public expectations of what government can and should do in response to emerging threats and future emergencies seem to be rising.

OBR: Tariffs, defence costs and ageing populations are all risks

A number of major global risks to the UK economy have “crystallised”, the Office for Budget Responsibility warns.

Its singles out Donald Trump’s trade war, and Russia’s invasion of Ukraine, saying:

In particular, as foreshadowed in our 2022 report, rising geopolitical tensions have given rise to the largest increase in effective global tariff rates in over a century and put the UK and other European countries under pressure to increase defence spending to their highest levels since the end of the Cold War.

The OBR also cites rising pensions and healthcare costs, saying;

Over the long term, the demographic pressures of an ageing population and rising costs of healthcare and other age-related expenditures are still, on current policy settings, projected to push borrowing above 20 per cent and debt above 270 per cent of GDP by the early 2070s.

OBR warns UK public finances are in a vulnerable position

Newsflash: The UK public finances have fallen into a “relatively vulnerable position” and are facing mounting risks, the country’s fiscal watchdog is warning.

The Office for Budget Responsibility has just issued its latest Fiscal risks and sustainability report. It warns that the UK’s ability to respond to future shock has been substantially eroded, with underlying public debt is now at its highest level since the early 1960s and projected to rise further.

The OBR says:

Efforts to put the UK’s public finances on a sustainable footing after a series of global shocks have met with only limited and temporary success in recent years, leaving the UK with the sixth-highest debt, fifth-highest deficit, and third-highest borrowing costs among 36 advanced economies.

Against this more vulnerable backdrop, the risks to the fiscal outlook are mounting, including: the sustainability of state and private pensions and the sector’s demand for government debt; risks to assets and liabilities on the public balance sheet and the Government’s new net financial liabilities target; and the combined costs of climate damage and the net zero transition.

The OBR’s report paints a concerning position about the UK pubic finances, showing the challenge facing chancellor Rachel Reeves.

It points out that:

-

at the end of last year, the UK government’s deficit was 5.7% of GDP, around 4 percentage points higher than the advanced-economy average. This is the third highest among 28 advanced European economies, and the fifth highest among 36 advanced economies – after France, Slovakia, the US, and Israel.

-

At 94% of GDP, UK government debt is the fourth highest among advanced European economies, and the sixth highest among advanced economies (after Japan, Greece, Italy, France, and the US).

-

And with its 10-year bond yielding 4.5% at the end of June, the UK government faces the third-highest borrowing costs of any advanced economy after New Zealand and Iceland.

New trade war deadline creates instability, UN trade agency says

The Trump administration’s decision to extend a negotiating deadline for tariff rates to 1 August is prolonging the period of uncertainty and instability for countries, the executive director of the United Nations trade agency has warned.

Pamela Coke-Hamilton, executive director of the International Trade Centre, told reporters in Geneva:

“This move actually extends the period of uncertainty, undermining long-term investment and business contracts, and creating further uncertainty and instability.”

Trump’s policies do not add up to a coherent strategy, fears Holger Schmieding, chief economist at Berenberg.

He fears the new US tariffs will weaken the country, explaining:

On the one hand, his administration is perceiving China as the key geopolitical threat to US interests. Underscoring that point, Trump has threatened to levy additional tariffs of 10% on all countries that align themselves with the fragile “BRICS” alliance of non-Western countries.

On the other hand, his new threats of 25% tariffs on Japan and South Korea can only hurt the relationship with these countries. Both Japan and South Korea are close geopolitical allies of the US right next door to China. Both had tried hard to strike deals with the US in recent weeks. They may well succeed in doing so before the new 1 August deadline.

But Trump’s narrow “America first” approach once again puts unnecessary stress on alliances that the US will need for any coherent geopolitical strategy. With tariffs, policy uncertainty and disrespect for multinational institutions and allies, Trump weakens the economic and geopolitical position of the US.

Goldman Sachs lifts forecast for US stock market

Overnight, Goldman Sachs has lifted its forecast for the US S&P 500 share index.

Goldman is now forecasting a 3% gain on the S&P 500 over the next three months, to 6,400 points, and an 11% gain in 12 months time, to 6,900 points.

It cites expectations of U.S. interest rate cuts and continued fundamental strength of major large-cap stocks as key drivers of its positive outlook, meaning it has lifted its price/earnings forecast.

The bank told clients:

Earlier and deeper Fed easing and lower bond yields than we previously expected, continued fundamental strength of the largest stocks, and investors’ willingness to look through likely near-term earnings weakness support our revised S&P 500 forward P/E forecast of 22x (from 20.4x).

The International Chamber of Commerce is hoping to see “positive movement” on trade talks in the coming days, now that Donald Trump has set new tariffs on some US trading partners.

John Denton, secretary general of the International Chamber of Commerce, says:

It is clear that the threat of punitive tariffs will remain on the table for some of America’s largest trading partners. Our hope is that the letters being sent this week will fire the starting gun for a concerted effort secure win-win deals — providing a true reset for global trade relations and removing the cloud of uncertainty currently hanging over major investment decisions.

The indication from the Administration that smaller economies will have their tariffs fixed at the baseline 10% rate is extremely welcome from a global development perspective.

While the situation is clearly fluid, we’re hoping to see some positive movement in the days ahead — not just to keep tariffs low, but to bring back some much-needed certainty for business operations and investment.

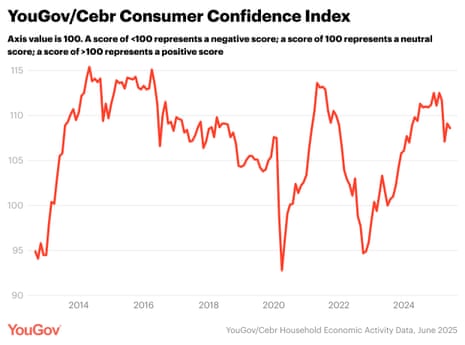

UK consumer confidence has dipped as workers worry that business activity is deteriorating, a new survey from YouGov shows.

The overall index of UK consumer morale, produced by YouGov and the Centre for Economics and Business Research (Cebr), dipped by 0.5 points in June, to 108.6 points.

Worsening perceptions of business activity among workers dragged the index down, countering an improvement in confidence about househod finances.

The survey also found:

-

Business activity measures for the past 30 days (-3.3) and next 12 months (-2.3) fell

-

Workers felt worse about their job security over the past 30 days (-3.0), although outlook improved (+1.3)

-

Measures tracking retrospective opinion of household finances (+0.8) and outlook for the next 12 months (+1.4) rose

The markets are shrugging at Trump’s latest tariff announcements, reports Bill Blain, market strategist at Wind Shift Capital.

Blain points out:

A year ago the idea a sovereign nation would blithely impose crippling global tariffs on its long-established friends, allies and competitors, and expect them to bend over and say; “thank you sir, can I have some more…” would be dismissed as the mad haverings of a dystopian crackpot….

Today it’s happening and no one bats an eyelid.

That’s because markets have concluded that last night’s tariffs are “just another TACO Trump ploy”, he adds:

Deals will get done, and resumed its upwards trajectory. The bottom line is no one expects the global trading economy to disappear in a sudden puff of logic because Trump delights in throwing spanners in the works.

History shows global trade is resilient to both hot and cold conflict, and swiftly adapts.

European stock markets have also opened higher, led by Germany.

The German DAX index rose by 50 points, or 0.2%, to 24,125, in early trading, amid some relief that European negotiators have another three weeks to reach a trade deal with Washington.

France’s CAC has inched up by 0.1%, with Spain’s IBEX gaining 0.14%.

Jochen Stanzl, chief market analyst at CMC Markets, says:

Donald Trump has once again retreated from imposing tariffs, allowing the DAX to rise above the 24,000-point mark. It appears that investors are eager to test the previous week’s highs once more, but the success of this endeavor will depend on the daily news regarding trade policy, which is expected to remain volatile. The trade issue continues to be a source of uncertainty for the stock market, and without a trade agreement with the U.S., a sustainable continuation of the rally could prove challenging.

This morning, the European Union faces both positive and negative news. On the positive side, the pause on tariffs has been extended until August. Trump seems to be sticking to his pattern of initially making threats before showing a willingness to negotiate. He likely understands that implementing reciprocal tariffs would be more harmful than beneficial to the ongoing discussions.

However, the negative aspect is that sector-specific tariffs on cars, auto parts, aluminum, and steel will remain in effect until August 1. This latest development is not cause for great celebration, as the EU has struggled to effectively counter the already high tariffs that are currently in place during the negotiations.”