.png) 1 month ago

26

1 month ago

26

Introduction: Oil on track for steepest weekly drop in 3.5 months

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

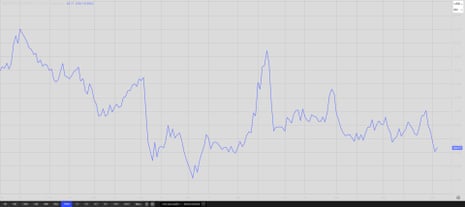

The oil price is on track for its steepest weekly drop in three and a half months, as crude prices slide to a four-month low.

Predictions that the OPEC+ group will keep increasing oil output have pushed down energy prices in the last few days.

Brent crude, the international benchmark, has fallen 8% so far this week – from $70.13 per barrel last Friday night to $64.59 per barrel today, and yesterday hit its lowest level since 2 June.

OPEC+ are due to meet on Sunday, and could hike output further despite concerns that the oil market is already oversupplied.

Unicredit analysts says the alliance of oil producers is expected to approve a further 137,000b/d increase in output on Sunday.

This would extend “its gradual pivot from price defence to market-share expansion” Unicredit say, adding:

Talk of larger increases has surfaced, but these appear improbable. Quotas have risen by over 2.5mb/d since April, and Brent crude has largely hovered around USD 67/bbl in recent weeks, with geopolitical events – from Israeli strikes in Doha to Ukrainian drone attacks – having had only fleeting impacts on pricing. This suggests oil markets are predominantly shaped by structural dynamics.

Falling oil prices are boost for consumers, and many businesses, and might also reassure central bankers that inflationary pressures will ease.

JPMorgan analysts said in a note:

“We believe September marked a turning point, with the oil market now heading towards a sizeable surplus in Q4 2025 and into next year.”

The agenda

-

8.30am BST: UN FAO food price index

-

9am BST: Eurozone service sector PMI report for September

-

9.30am BST: UK service sector PMI report for September

-

9.30am BST: ONS: The impact of the motherhood penalty on monthly employee earnings and employment status in England

-

10.40am BST: ECB President Lagarde speaks at the Klaas Knot farewell symposium

-

2.20pm BST: Bank of England governor Andrew Bailey gives keynote speech at the Klaas Knott farewell symposium, ‘Macro-financial stability in a fragmenting world’

Key events Show key events only Please turn on JavaScript to use this feature

RAC: Pump prices creep back up

Despite the downward pressure on the oil price in rcent months, drivers are facing rising prices at the pumps.

Motoring body the RAC has reported that petrol and diesel prices rose by around a penny a litre during September, even though crude prices were effectively flat during the month.

RAC Fuel Watch data shows that the average price of a litre of unleaded petrol went up from 134.64p to 135.41p (+0.77p) while diesel increased from 142.19p to 143.14p (+0.95p).

The RAC point out that fuel prices have risen in eight of the past 12 months but are still well below the highs seen in late February (when petrol hit a 12-month peak of 139.65p per litre).

RAC head of policy Simon Williams argues that price increases are unjustifiable:

“Sadly, pump prices crept up by a penny a litre in September reversing the drop drivers saw in August.

The fact prices have risen at all was made worse by the fact that there was little to no movement in the price of oil, or the pound-to-dollar exchange rate – the prime determiners of fuel prices – and therefore seemingly no justifiable reason for an increase.

Last week, the UK’s competition watchdog said it was “deeply concerned” by signs that companies have ramped up profits at the expense of consumers.

Williams says:

“It was also disappointing to have the Competition and Markets Authority confirm what we have known for some time that retailer margins remain above historic levels. We’re grateful for this level of scrutiny, but it appears yet to have had the effect on retailer behaviour we’d hoped it would.

The comparison with average prices and margins in Northern Ireland makes the point that it is possible to sell fuel more cheaply and still make money.

Introduction: Oil on track for steepest weekly drop in 3.5 months

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

The oil price is on track for its steepest weekly drop in three and a half months, as crude prices slide to a four-month low.

Predictions that the OPEC+ group will keep increasing oil output have pushed down energy prices in the last few days.

Brent crude, the international benchmark, has fallen 8% so far this week – from $70.13 per barrel last Friday night to $64.59 per barrel today, and yesterday hit its lowest level since 2 June.

OPEC+ are due to meet on Sunday, and could hike output further despite concerns that the oil market is already oversupplied.

Unicredit analysts says the alliance of oil producers is expected to approve a further 137,000b/d increase in output on Sunday.

This would extend “its gradual pivot from price defence to market-share expansion” Unicredit say, adding:

Talk of larger increases has surfaced, but these appear improbable. Quotas have risen by over 2.5mb/d since April, and Brent crude has largely hovered around USD 67/bbl in recent weeks, with geopolitical events – from Israeli strikes in Doha to Ukrainian drone attacks – having had only fleeting impacts on pricing. This suggests oil markets are predominantly shaped by structural dynamics.

Falling oil prices are boost for consumers, and many businesses, and might also reassure central bankers that inflationary pressures will ease.

JPMorgan analysts said in a note:

“We believe September marked a turning point, with the oil market now heading towards a sizeable surplus in Q4 2025 and into next year.”

The agenda

-

8.30am BST: UN FAO food price index

-

9am BST: Eurozone service sector PMI report for September

-

9.30am BST: UK service sector PMI report for September

-

9.30am BST: ONS: The impact of the motherhood penalty on monthly employee earnings and employment status in England

-

10.40am BST: ECB President Lagarde speaks at the Klaas Knot farewell symposium

-

2.20pm BST: Bank of England governor Andrew Bailey gives keynote speech at the Klaas Knott farewell symposium, ‘Macro-financial stability in a fragmenting world’