.png) 3 months ago

52

3 months ago

52

Oil price shock likely to 'push the UK economy into recession'

The oil price shock hitting the global economy could push the UK into recession, Tomasz Wieladek, chief European macro economist at investment managent firm T. Rowe Price, is warning this morning.

Wieladek says the UK’s economy’s failure to grow in January show that it was weak even before the oil shock, which is likely to hit consumer spending and create more cost of living pressures.

Following today’s weaker-than-expected GDP report, Wieladek writes:

UK GDP growth stagnated in January, far weaker than market expectations of a 0.2% month-on-month pickup. The weakness was driven by services, the main part of the UK economy, and can be partially explained by tight monetary policy and the fiscal policy consolidation the UK is currently experiencing. Both of these policies are reducing demand, and the data is beginning to show it. Furthermore, AI is likely reducing hiring in the services sector, which in turn is leading to higher unemployment and softer demand. Overall, the UK economy has been weak ahead of the most recent oil shock.

The war in the Middle East and the consequent oil price rise will raise inflation and reduce consumer spending. The associated tightening in financial conditions we have seen in the bond market will exacerbate these effects. There will be significant demand destruction going forward.

The UK has been one of the weakest advanced economies in terms of recent growth performance. Therefore, the current oil price shock will most likely not just lead to inflation, but also push the UK economy into recession, raising unemployment and reducing GDP. Stagflation is just around the corner.

This puts the Bank of England (BoE) into a difficult position, he adds:

On the one hand, the BoE’s inflation-target credibility has weakened, as UK inflation has been higher and more persistent than elsewhere. On the other hand, a recession is likely. What should the BoE do? The key to easing financial conditions and supporting the recovery from the recession is to ease the current financial tightening. The best way to achieve this is to keep policy tight and publicly commit to reaching the 2% target at all costs.

A hawkish approach to monetary policy can kill two birds with one stone in this situation. Inflation credibility can be restored, and financial conditions will ease, as inflation risk premia get priced out. The BoE should keep rates on hold and prepare the public for the prospect of further hikes.

Key events Show key events only Please turn on JavaScript to use this feature

Housebuilder Berkeley flags risk from Middle East crisis

British homebuilder Berkeley Group has warned that the Iran war could hurt the UK economy.

Berkeley reaffirmed its pre-tax profit guidance for the year this morning in a trading update, before flagging that it hasn’t yet seen the impact of the crisis on the housing market.

It told shareholders:

The trading environment over this period has remained constrained by the impact on consumer confidence of geo-political events and macro-economic uncertainty. However, sales enquiries remain good and the value of underlying reservations has been recovering towards the levels seen over the summer prior to the pre-Budget hiatus.

The emerging situation in the Middle East is weighing heavily on risk sentiment and we await to see the impact of this on the market. While reaffirming guidance, we are aware of the risk of a further deterioration in macro conditions with the potential for higher inflation in the near term and for interest rates to remain higher for longer.

Berkeley’s shares are down 3% this morning, putting it among the top fallers on the FTSE 100 index.

UK assets falling

The pound, and the UK stock market, are both falling this morning.

Sterling is down three-quarters of a cent against the US dollar at $1.3263, approaching the three-month low set last week.

The FTSE 100 index of blue-chip shares is down too – losing 58 points or 0.56% at 10,247 points.

The more domestically focused FTSE 250 index is down 0.7%.

Matt Britzman, senior equity analyst at Hargreaves Lansdown, says:

“UK markets opened lower this morning, weighed down by a softer‑than‑expected GDP print and ongoing tensions in the Middle East. The economy failed to grow at all in January, suggesting activity was already subdued even before the recent jump in energy prices began to bite.

That’s starting to force a rethink of this year’s outlook, with previous 1.0% growth expectations now looking optimistic - with some scenarios pointing to closer to 0.6%, 0.4% or even 0.1%, depending on how long elevated energy costs stick around.

IoD: Stalling UK economy vulnerable to fallout from conflict in the Middle East

The outbreak of conflict in the Middle East hits an “already troublingly fragile UK economy” and sharpens the need for action to lift growth prospects, says Anna Leach, chief economist at the Institute of Directors.

Energy prices have already risen sharply, and unprecedented damage to supply capacity in the Middle East will have uncertain effects on energy prices longer term.

This risks driving up costs for businesses and consumers at a point when inflation was only just heading back to target, and could cause a further slump in confidence and impetus to spend. It is right that the government stands ready to intervene and support the economy once again.

But short-term agility must not distract from the UK’s longer term growth needs. From an energy strategy which takes a realistic approach to the transition to net zero, to workers’ rights that avoid overburdening employers, a laser focus on growth is urgently needed.”

Oil price shock likely to 'push the UK economy into recession'

The oil price shock hitting the global economy could push the UK into recession, Tomasz Wieladek, chief European macro economist at investment managent firm T. Rowe Price, is warning this morning.

Wieladek says the UK’s economy’s failure to grow in January show that it was weak even before the oil shock, which is likely to hit consumer spending and create more cost of living pressures.

Following today’s weaker-than-expected GDP report, Wieladek writes:

UK GDP growth stagnated in January, far weaker than market expectations of a 0.2% month-on-month pickup. The weakness was driven by services, the main part of the UK economy, and can be partially explained by tight monetary policy and the fiscal policy consolidation the UK is currently experiencing. Both of these policies are reducing demand, and the data is beginning to show it. Furthermore, AI is likely reducing hiring in the services sector, which in turn is leading to higher unemployment and softer demand. Overall, the UK economy has been weak ahead of the most recent oil shock.

The war in the Middle East and the consequent oil price rise will raise inflation and reduce consumer spending. The associated tightening in financial conditions we have seen in the bond market will exacerbate these effects. There will be significant demand destruction going forward.

The UK has been one of the weakest advanced economies in terms of recent growth performance. Therefore, the current oil price shock will most likely not just lead to inflation, but also push the UK economy into recession, raising unemployment and reducing GDP. Stagflation is just around the corner.

This puts the Bank of England (BoE) into a difficult position, he adds:

On the one hand, the BoE’s inflation-target credibility has weakened, as UK inflation has been higher and more persistent than elsewhere. On the other hand, a recession is likely. What should the BoE do? The key to easing financial conditions and supporting the recovery from the recession is to ease the current financial tightening. The best way to achieve this is to keep policy tight and publicly commit to reaching the 2% target at all costs.

A hawkish approach to monetary policy can kill two birds with one stone in this situation. Inflation credibility can be restored, and financial conditions will ease, as inflation risk premia get priced out. The BoE should keep rates on hold and prepare the public for the prospect of further hikes.

Markets expecting UK interest rates to rise next

Despite the lack of growth in January, and fears over the outlook for the year, hopes that the Bank of England might cut interest rates to support the economy have faded.

Since the Iran war began, the odds of a rate cut next week have collapsed from 80% to single figures. This morning, the money markets say there’s a 96.5% chance that the BoE holds rates at 3.75% next Thursday.

Looking ahead, there’s more chance of a rate rise than a cut by Christmas. The markets are predicting a 20 basis point (0.2 percentage point) rise in rates by December, which suggests there’s more than 80% chance of a quarter-point rise in rates by then.

A rate cut is fully priced in by June 2027.

Bank policymakers will need to judge the wisdom of sitting on their hands and allowing the energy shock the wash through the economy (higher rates won’t get more oil through the strait of Hormuz!), versus the risk of letting inflation expectations to jump.

The Iran war is a “growing downside risk” to the UK economy, warns Andrew Hunter, associate director and senior economist at Moody’s Analytics:

“The latest monthly GDP data suggest that the U.K. economy was continuing to struggle at the start of the year, with GDP experiencing no growth in January after only marginal gains in previous months.

The improvement in the PMI surveys suggests growth should pick up over the coming months and we expect growth over the first quarter as a whole to be slightly stronger, but there is a growing downside risk that the conflict in the Middle East will drive a sharper rise in inflation and deal a renewed blow to consumer and business confidence.”

Hoped for 'stability dividend' now unlikely

The lack of growth in January suggests that Rachel Reeves’s autumn budget has not given the economy a brisk pick-me-up.

There had also been hopes for a ‘stability dividend’ after the chancellor’s news-lite spring forecast thi smonth, this seems unlikely too – with the Iran war now threatening the economy.

Raj Badiani, economics director at S&P Global Market Intelligence, says:

“GDP growth strengthened moderately in the three months to January when compared to the previous three months, led by improving services output, released from the uncertainty that accompanied the 2025 Autumn Budget. However, the outlook has darkened with the hoped for “stability dividend” from a low-key Spring Statement unlikely to materialise. Furthermore, the economy is vulnerable to a growth downgrade for this year because of the war in the Middle East and the resulting spike in energy costs.

“We had previously assumed that economic conditions would improve in the second half of this year but the prospect of higher energy bills, a renewed rise in inflation and a pause in monetary policy easing are likely to hit business and consumer activity. A key risk is that households, fearful of a prolonged spike in energy costs, raise their precautionary saving.

RSM: UK economy enters the energy crisis with no momentum

Today’s GDP report shows the UK economy entered the energy crisis with no momentum, warns Thomas Pugh, chief economist at audit, tax and consulting firm RSM UK.

Pugh explains:

“Zero growth in January highlights just how little momentum the economy had coming into the energy crisis. That makes it more likely that growth will dip sharply below 1% this year, even if there is a swift resolution to the crisis.

“Stagnation in January would make us worried about growth this year, even without the energy price shock that will start to show up in the March data. Indeed, the big improvement in survey data at the start of the year doesn’t seem to have carried over into stronger activity. Improved retail sales were offset by a sharp drop in hospitality activity, suggesting consumers are still cautious.

And the moribund employment and housing market clearly showed up in a 5.7% drop in employment activities, and a 3.9% drop in leasing activities. We had been expecting both these factors to improve over the rest of the year, but the sharp rise in borrowing costs and uncertainty makes that unlikely now.

NIESR: This is a worrying start

The UK’s failure to grow in January is a “worrying start” to 2026, reports Fergus Jimenez-England, associate economist at the National Institute of Economic and Social Research (NIESR).

Jimenez-England says:

“GDP did not grow in January, despite surveys pointing to a revival in business sentiment early in the New Year. Services stagnated while production entered its second month of contraction.

This is a worrying start to the quarter, given that the early-year improvement in business confidence is likely to be short-lived as global disruption linked to the Iran War hits the UK economy.

We expect the impact on growth in the first quarter to be limited, but if energy prices remain elevated for the rest of the year it could reduce GDP growth by around 0.2 percentage points in 2026.”

Reeves: We have the right economic plan

Chancellor of the Exchequer Rachel Reeves has responded to this morning’s GDP report, saying:

“Our economic plan is the right one, but I know there is more to do.

In an uncertain world, we are building a stronger and more secure economy by cutting the cost of living, cutting national debt and creating the conditions for growth to make all parts of the country better off.”

Employment activities fell in January

There was also a worrying decline in recruitment activity in January.

The ONS report there was a 5.7% fall in employment activities during the month – suggesting a decline in hiring by UK businesses at the start of this year.

The fall in employment activities was the largest negative contribution from a single industry to both services output and real GDP growth in January.

Many employment groups have blamed the government’s decision to increase employer national insurance contributions, and the minimum wage, for hitting recruitment.

It might even be a sign that artificial intelligence is now hitting the recruitment market, wiping out some job opportunities….

Estate agent activity slumped

A slump in the property sector hurt the economy over the three months to January.

The ONS reports that there was a 7.1% drop in “real estate activities on a fee or contract basis” over the quarter.

On an annual basis, UK GDP is estimated to be 0.8% higher in January 2026, compared with January 2025.

That’s quite a poor performance in historic terms.

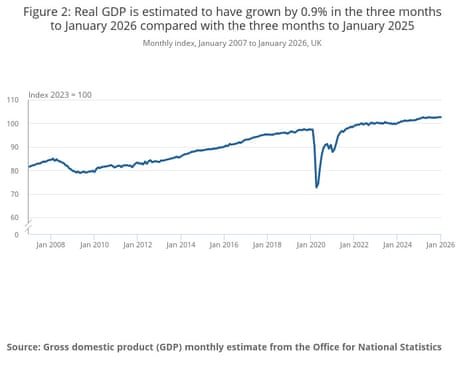

UK grew 0.2% in last three months

Over the three months to January, the UK economy grew by 0.2%, up from growth of 0.1% in the three months to December.

That’s partly because activity picked up at JLR’s car factories, after a damaging cyber attack that halted production last September.

ONS director of economic statistics, Liz McKeown, says:

“Growth ticked up slightly in the latest three months, partly reflecting the recovery of car manufacturing, following the cyber incident in the Autumn. Within services, which also increased, wholesale continued to rebound from a weak summer. However, the overall picture remains subdued, with no growth in the latest month.

“There was another large fall in the construction industry in the latest three months, with continued contraction in housebuilding.”

UK economy failed to grow in January

Newflash: The UK economy stagnated in January, stumbling even before the Iranian war drove up energy prices.

The Office for National Statistics reports that UK GDP was unchanged in January, dashing hopes of 0.2% growth.

It says that in January:

-

Monthly GDP showed no growth, following growths of 0.1% in December and 0.2% in November 2025.

-

Services showed no growth, production fell by 0.1%, and construction grew by 0.2% in January 2026.

That suggests the economy was weaker than thought even before the threat of an energy price shock.

Brent crude oil is still trading over $100 a barrel this morning, having climbed since the Iran war started almost two weeks ago.

Introduction: UK GDP report for January

Good morning, and welcome to our rolling coverage of business, the financial markets, and the world economy.

A lot has changed since January – with conflict in the Middle East driving oil prices to $100 a barrel, disrupting supply chains and fuelling stagflation fears.

So the latest gauge of the health of the British economy may be out of date even before it is delivered to us this morning.

The latest UK GDP report, due at 7am, is expected to show a pick-up in growth in the first month of 2026. Economists predict the economy will have grown by 0.2% in the month, up from 0.1% in December.

In more normal times, Rachel Reeves would be able to trumpet this as a sign that the recovery was gaining ground. But fears of an energy price shock means ministers should temper any enthusiasm.

Sanjay Raja, Deutsche Bank’s chief UK economist, explains:

After a disappointing end to the year, we expect the economy to jump to a flying start in Q1-26. Indeed, activity data has thus far been encouraging. And we expect some catch up in the first couple of months of the year, after a weak Q4-25.

The upcoming GDP report won’t be front and centre for markets, however. Events in the Middle East continue to overshadow lagged data.

The unfolding energy shock will have important implications for inflation and thus real disposable incomes. Some signs of stabilisation in the labour market now look fragile. The path for interest rate cuts is now also in doubt. In short, uncertainty has picked up yet again. Growth risks are now almost single-handedly skewed to the downside - with inflation risks skewed to the upside.

The agenda

-

7am GMT: UK GDP report for January

-

7am GMT: UK trade report for January

-

10am GMT: Eurozone industrial production report for January

-

12.30pm GMT: US PCE inflation measure

-

2pm GMT: US JOLTs Job Openings report

-

2pm GMT: University of Michigan’s survey of US consumer confidence